How to Qualify for a Home Loan USA is a crucial topic for anyone looking to purchase a home. Lenders evaluate your credit score, income stability, debt-to-income ratio, and savings before approving a mortgage. Understanding How to Qualify for a Home Loan USA helps you prepare your finances, gather required documents, and avoid common mistakes during the application process. A strong credit profile and steady employment can improve your chances of approval and secure better interest rates. By learning How to Qualify for a Home Loan USA, you can confidently take the first step toward homeownership and make smarter financial decisions.

Understanding Debt in the US

Types of Debt Americans Face

In the United States, debt comes in many forms. The most common types include credit card debt, student loans, auto loans, mortgages, and personal loans. Each type carries different interest rates and repayment structures. Credit cards often have the highest interest rates, making them a priority when planning how to pay off debt fast (US strategy).

Student loans, on the other hand, usually have lower interest rates but longer repayment periods. Mortgages are considered “good debt” because they help build equity, but they still require careful management.

Interest Rates and Their Impact

Interest rates are the silent factor that can either speed up or slow down your debt repayment. High-interest debts grow quickly, making it harder to reduce the principal balance. That’s why understanding interest rates is critical when choosing a repayment strategy.

Why Paying Off Debt Quickly Matters

Financial Freedom Benefits

When you eliminate debt, you free up your income for savings, investments, and personal goals. You’re no longer tied down by monthly obligations, which creates peace of mind and flexibility.

Credit Score Improvement

Paying off debt improves your credit utilization ratio, which is a major factor in your credit score. A better score means better loan terms, lower interest rates, and more financial opportunities.

Create a Clear Debt Inventory

Listing All Debts

Start by writing down every debt you owe. Include the lender, balance, interest rate, and minimum payment. This gives you a clear picture of your financial situation.

Calculating Total Balance

Add everything together to determine your total debt. This number might feel intimidating, but it’s the first step toward taking control.

Choose the Best Payoff Strategy

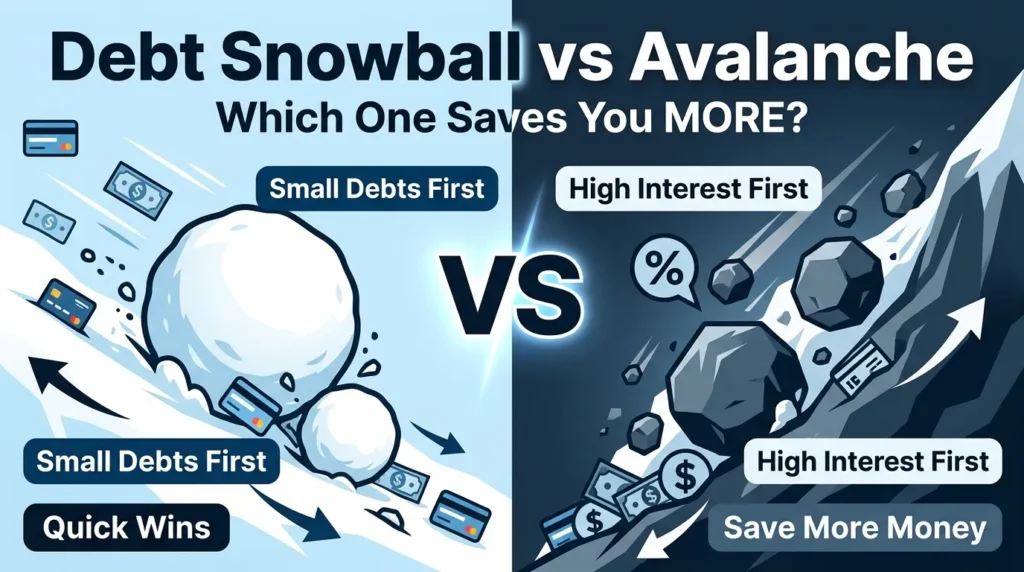

Debt Snowball Method

This method focuses on paying off the smallest debts first. You gain quick wins, which boosts motivation. Once a debt is cleared, you roll that payment into the next one.

Debt Avalanche Method

Here, you target debts with the highest interest rates first. This approach saves more money over time and is often recommended in most How to Pay Off Debt Fast (US Strategy) plans.

Build a Realistic Budget Plan

Tracking Income and Expenses

A budget helps you understand where your money goes. List all income sources and track every expense, including small purchases.

Cutting Unnecessary Costs

Cancel unused subscriptions, reduce dining out, and limit impulse purchases. Even small changes can free up extra cash for debt payments.

Increase Your Income Streams

Side Hustles in the US

Popular side hustles include ridesharing, food delivery, online tutoring, and selling products on platforms like Etsy or eBay.

Freelancing Opportunities

If you have skills like writing, graphic design, or coding, freelancing can significantly boost your income and accelerate debt repayment.

Negotiate Lower Interest Rates

Talking to Creditors

Many people don’t realize they can negotiate interest rates. A simple phone call to your lender can sometimes reduce your rate, saving you money.

Balance Transfer Options

Transferring your balance to a card with a 0% introductory APR can help you pay off debt faster without accumulating interest.

Use Windfalls Wisely

Tax Refund Strategy

Instead of spending your tax refund, use it to pay down debt. This can make a significant dent in your balance.

Bonuses and Extra Cash

Any unexpected income should go directly toward debt repayment rather than lifestyle upgrades.

Avoid Common Debt Mistakes

Minimum Payment Trap

Paying only the minimum keeps you in debt longer and increases the total interest paid.

Accumulating New Debt

Avoid using credit cards while paying off existing balances. Otherwise, you’ll undo your progress.

Automate Your Payments

Benefits of Automation

Automation ensures you never miss a payment and helps build discipline.

Tools and Apps

Use budgeting apps like Mint or YNAB to track progress and manage payments efficiently.

Consider Debt Consolidation

Personal Loans

Debt consolidation loans combine multiple debts into one payment, often with a lower interest rate.

Pros and Cons

While consolidation simplifies payments, it requires discipline to avoid accumulating new debt.

Stay Motivated During the Process

Setting Milestones

Break your journey into smaller goals. Celebrate each milestone to stay motivated.

Celebrating Wins

Reward yourself in small ways when you pay off a debt—just don’t overspend.

Emergency Fund Importance

Why It Matters

An emergency fund prevents you from falling back into debt when unexpected expenses arise.

How Much to Save

Start with $500–$1,000, then gradually build up to 3–6 months of expenses.

FAQs

1. What is the fastest way to pay off debt in the US?

The fastest way is using the debt avalanche method combined with increased income and strict budgeting.

2. Should I save or pay off debt first?

Start with a small emergency fund, then focus on paying off high-interest debt.

3. Is debt consolidation a good idea?

It can be helpful if it lowers your interest rate and simplifies payments.

4. How can I stay motivated while paying off debt?

Track progress, set goals, and celebrate small wins.

5. Can I negotiate my debt?

Yes, many creditors are willing to lower interest rates or offer payment plans.

6. How long does it take to become debt-free?

It depends on your income, debt amount, and strategy, but consistent effort speeds up the process.