Bank Fees Explained USA is a complete and easy-to-understand guide that helps you uncover the real costs hidden in everyday banking. This article breaks down Bank Fees Explained USA in detail, covering monthly maintenance fees, overdraft penalties, ATM charges, wire transfer costs, minimum balance fees, and other hidden banking expenses that can quietly drain your money. Designed for students, professionals, and everyday account holders, this guide simplifies complex banking terms into clear, practical insights. With Bank Fees Explained USA, you will learn proven strategies to reduce or completely avoid unnecessary charges by choosing the right bank accounts, using fee-free ATM networks, and managing your finances more efficiently. This resource empowers you to make smarter financial decisions, protect your savings, and build stronger money habits. If you want to fully understand Bank Fees Explained USA and take control of your banking costs, this guide is your essential financial tool for smarter money management and long-term savings success

What Are Bank Fees?

Bank fees are charges that financial institutions impose for the services they provide. These fees are applied for different purposes, including account maintenance, transactions, overdrafts, or optional services such as wire transfers. While some fees are straightforward, others are hidden or may not apply under certain conditions. Understanding these charges is crucial because they can affect your account balance, reduce your savings, and even impact your credit score if left unmanaged.

Financial institutions have varying fee structures, and the amounts depend on the type of account, the bank’s policies, and your usage habits. For example, a checking account may charge a monthly maintenance fee unless you meet a minimum balance requirement, while a savings account may charge for exceeding withdrawal limits. Knowing the fee structure of your accounts helps you avoid surprises and make cost-effective banking decisions.

Understanding Banking Charges in the USA

Banks in the USA offer a wide range of accounts and services, each with different fees and rules. Most financial institutions charge fees for operational costs, including maintaining accounts, processing transactions, and providing additional services. These fees are often applied automatically, which makes it important for account holders to monitor their accounts regularly.

Banking regulations in the USA require banks to disclose fees, but they are sometimes buried in account agreements or legal documents. Therefore, reading these agreements carefully is essential. By understanding banking charges, you can identify fee-waiving opportunities, choose the right accounts, and avoid unnecessary costs.

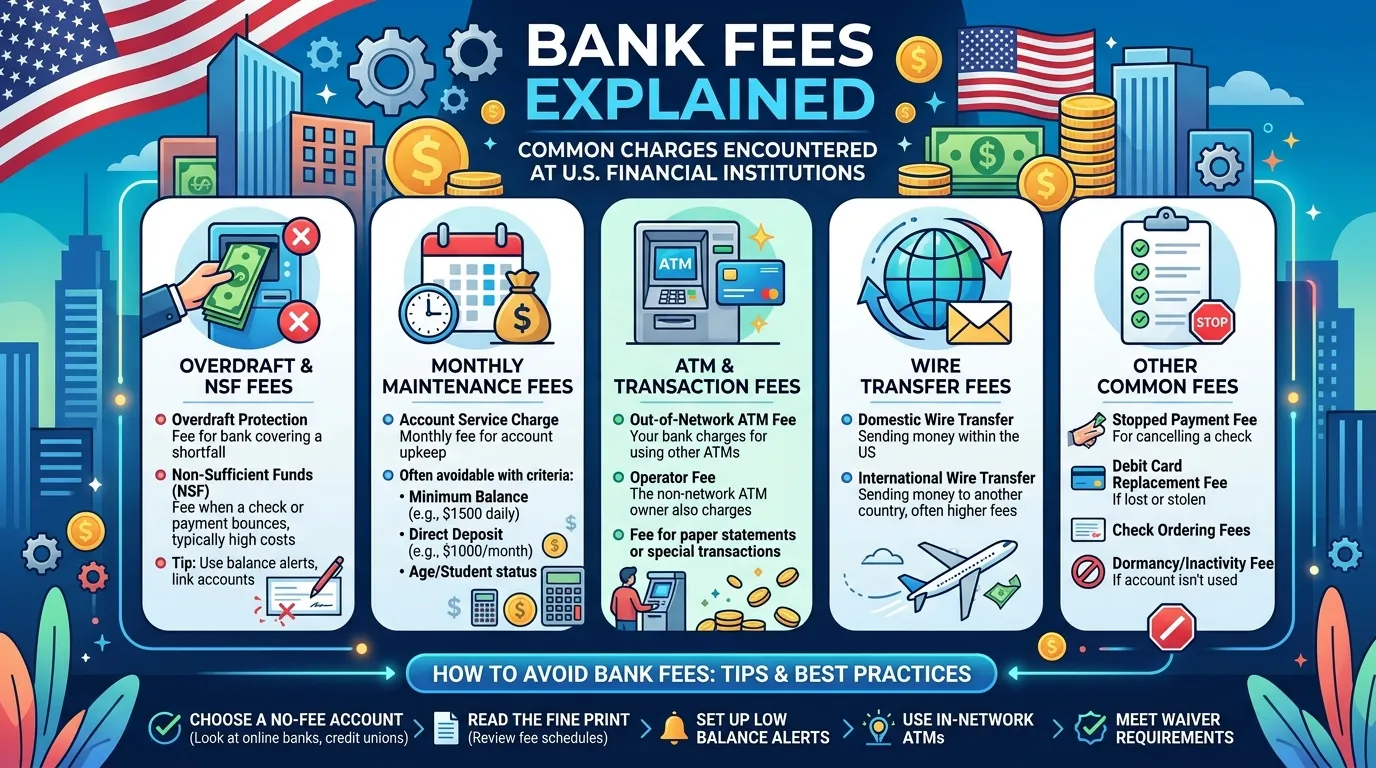

Common Types of Bank Fees in the USA

Monthly Maintenance Fees

Monthly maintenance fees are the most common type of bank charge. These fees are typically applied to checking and savings accounts for maintaining your account. The amount varies by bank and can range from $5 to $25 per month. Some banks waive this fee if you meet specific conditions, such as maintaining a minimum balance, receiving direct deposits, or using electronic statements.

For example, a checking account may charge a $12 monthly maintenance fee, but if you maintain a $1,000 balance or have a monthly direct deposit of $500, the fee may be waived. Understanding the rules for fee waivers allows you to manage your account efficiently and reduce unnecessary expenses.

Overdraft Fees Explained

Overdraft fees occur when you spend more money than is available in your account, and the bank covers the difference. Overdraft fees can range from $25 to $35 per transaction, and repeated overdrafts can become a significant financial burden.

Many banks offer overdraft protection services that link a savings account or line of credit to cover overdrafts. While this service can prevent declined transactions, it may also include fees. To avoid overdraft fees, monitor your account balance regularly, set up low-balance alerts, and plan your expenses carefully.

For example, if you have $50 in your checking account and spend $70, your bank may charge an overdraft fee of $35. By linking your savings account for overdraft protection, you can avoid declined transactions, but some banks may charge a smaller transfer fee.

ATM Withdrawal Fees

Using ATMs outside your bank’s network is another common source of fees. Banks typically charge $2 to $5 per withdrawal, and the ATM operator may also charge a fee. Frequent withdrawals from out-of-network ATMs can accumulate quickly, reducing your account balance over time.

To minimize ATM fees, use ATMs within your bank’s network, consider online banks with nationwide fee-free ATMs, or consolidate cash withdrawals to reduce the number of transactions. Some banks also reimburse a limited number of out-of-network ATM fees per month, which can be a valuable feature if you travel frequently.

Minimum Balance Fees

Certain accounts require you to maintain a minimum balance to avoid monthly fees. Falling below the minimum balance can result in a monthly penalty, which can range from $5 to $25. Monitoring your account regularly ensures you stay above the required minimum balance.

For example, if your account requires a $500 minimum balance and your balance drops to $450, you may be charged a $10 fee. Regularly reviewing your balance and setting reminders to maintain the required amount can prevent these fees.

Credit Card Fees

Credit card fees differ from checking and savings account fees but are important to consider. Common charges include annual fees, late payment fees, balance transfer fees, and foreign transaction fees. Paying your credit card balance on time and choosing cards without unnecessary fees can save significant money.

For instance, a credit card with a $95 annual fee may offer perks that justify the cost, such as cash-back rewards or travel benefits. Understanding the fee structure and selecting the right card for your spending habits can prevent unnecessary expenses.

Hidden Banking Fees You Should Watch For

Some bank fees are less obvious and can catch customers by surprise. Identifying these hidden fees helps prevent unexpected reductions in your account balance.

Foreign Transaction Fees

Foreign transaction fees apply when you use your debit or credit card outside the United States. These fees are typically 1% to 3% of the transaction amount and can add up quickly for frequent travelers. Choosing cards without foreign transaction fees or using multi-currency accounts can save money during international travel.

Paper Statement Fees

Some banks charge a fee for providing paper statements instead of electronic statements. This fee can range from $1 to $5 per month. Switching to online statements not only reduces costs but is also environmentally friendly.

Excessive Withdrawal Fees on Savings Accounts

Savings accounts may limit the number of withdrawals per month, often to six transactions under federal regulations. Exceeding this limit can result in service charges, which can reduce your savings over time. Monitoring your withdrawal activity and consolidating transfers can prevent these fees.

How to Avoid or Reduce Bank Fees

Bank fees are often unavoidable, but there are strategies to minimize them and optimize your banking experience.

Choose Fee-Free Banking Options

Many banks and credit unions offer accounts with no monthly maintenance fees. Online banks, in particular, often provide accounts with no minimum balance requirements and low-cost services. Comparing account options and selecting fee-free accounts is one of the simplest ways to save money.

Set Up Direct Deposits

Direct deposits can help you meet fee-waiving criteria for certain accounts. By arranging for your salary, government benefits, or other regular payments to be directly deposited, you can often avoid monthly maintenance fees and maintain account eligibility.

Monitor Your Account Regularly

Keeping track of your account balance and transactions helps prevent overdraft fees and ensures that you maintain minimum balance requirements. Many banks provide mobile apps and alert services to notify you of low balances or unusual activity.

Use In-Network ATMs

Limiting ATM withdrawals to in-network ATMs reduces fees. Planning cash withdrawals and consolidating transactions also minimizes the number of fees incurred over time.

Automate Savings and Transfers

Linking accounts for automatic savings and transfers ensures that you maintain required balances and avoid overdraft charges. Scheduled transfers also help you budget effectively and prevent unnecessary spending.

Understand Account Agreements

Reading and understanding your bank’s terms and conditions is critical. Familiarize yourself with fee structures, conditions for fee waivers, and services that may incur extra charges. Knowledge is the best defense against unexpected fees.

Online Banking vs. Traditional Banking Fees

The rise of online banking has changed the landscape of account management in the USA. Online banks often provide lower fees due to reduced overhead costs. They typically offer:

- Fee-free checking and savings accounts

- Nationwide ATM networks without extra charges

- Higher interest rates on savings

- Easy account management through mobile apps

Traditional brick-and-mortar banks, while convenient for in-person services, may have higher fees and lower flexibility. Comparing online and traditional banking options allows you to select an account that best suits your needs and minimizes costs.

Tips for Managing Your Bank Accounts Efficiently

Managing your bank accounts effectively ensures you avoid fees and maximize financial benefits. Here are some actionable tips:

- Track Your Balances: Monitor accounts daily or weekly to prevent overdrafts and maintain minimum balances.

- Automate Payments: Schedule recurring bills and payments to avoid late fees.

- Select the Right Account Type: Choose accounts that fit your banking habits and avoid unnecessary charges.

- Use Alerts: Set up notifications for low balances, pending transactions, and payment due dates.

- Review Statements Regularly: Check for errors, fraudulent charges, or unexplained fees.

- Consolidate Accounts: Reducing the number of accounts can simplify management and reduce fees.

- Plan Withdrawals: Limit ATM usage to fee-free machines or consolidate withdrawals to avoid multiple fees.

Frequently Asked Questions (FAQs)

1. What are the most common bank fees in the USA?

Common fees include monthly maintenance fees, overdraft fees, ATM withdrawal fees, minimum balance fees, and credit card fees.

2. How can I avoid overdraft fees?

Monitor account balances regularly, set up low-balance alerts, and link a savings account or line of credit for overdraft protection.

3. Are ATM withdrawal fees avoidable?

Yes, by using in-network ATMs, online banks with nationwide fee-free access, or consolidating cash withdrawals.

4. How do hidden fees affect my account?

Hidden fees like paper statement charges or foreign transaction fees can gradually reduce your balance. Regular account review prevents these surprises.

5. What is the difference between checking and savings account fees?

Checking accounts often have maintenance and overdraft fees, while savings accounts may charge for excessive withdrawals or low minimum balances.

6. Are online banks cheaper than traditional banks?

Typically, yes. Online banks have lower overhead costs and often provide fee-free accounts, higher interest rates, and flexible services.

7. Can I negotiate bank fees?

Some banks allow fee waivers or reductions, especially for loyal customers or those who maintain high balances. It’s worth contacting your bank to inquire.

8. How do direct deposits affect fees?

Direct deposits can help you meet requirements for waiving monthly maintenance fees and ensure eligibility for certain account benefits.

9. What is the safest way to avoid foreign transaction fees?

Use credit cards or debit cards designed for international travel with no foreign transaction fees, or use multi-currency bank accounts.

10. How often should I review my account statements?

Monthly review is essential, but weekly monitoring through mobile apps ensures timely detection of errors and prevents unexpected fees.